The Common Trait Bonds and Institutional Asset Owners Share

The risk profiles of bonds and decision makers at the typical institutional asset owner share a common, asymmetric, risk profile where downside risk often greatly outweighs the upside. Keeping that in mind can help shape how to effectively position a fixed income strategy within the competitive landscape.

Tom Coleman

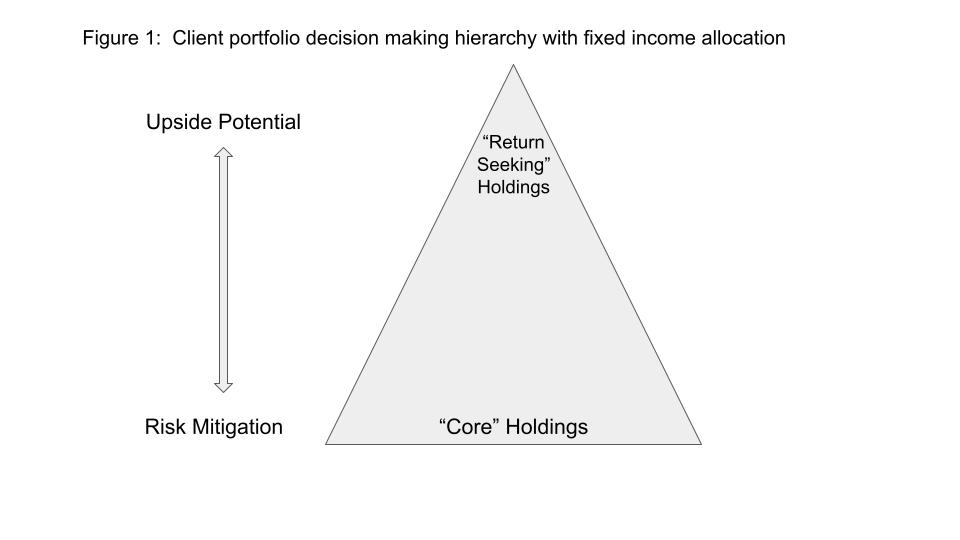

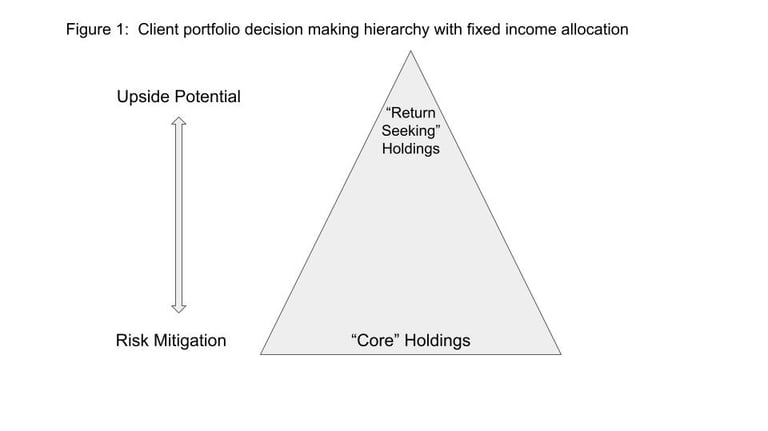

Remember that clients typically look at fixed income as a tool to mitigate risk, be it to hedge a liability stream, to dampen the volatility of higher risk/return assets in their portfolio, as a safe harbor in periods of volatility or as a source of steady income; in each case there is the draw of having more certainty in terms of outcomes that they are gaining in exchange for giving up some degree of upside. This translates to a pyramid shape of exposures in client portfolios, with the largest allocation to the risk mitigating “core” holdings and decreasing allocations to “return seeking” holdings as you trade risk mitigation for upside potential (Figure 1). The asset allocation composition of the pyramid will be dependent on a client’s portfolio objectives, overall asset allocation and risk profile.

The same logic often applies within manager selection within areas of fixed income specialization. Clients often start with what might be thought of as “safer” choices within a given allocation (eg., core, high yield, EMD) and add managers that bring added value to their overall structure. This helps explain why a manager like PIMCO appears in many clients’ core manager rosters: a long and proven performance record combined with the perceived “safety” that accompanies sticking with the crowd. For most other managers then, the objective should not be to topple PIMCO but rather to understand what the client might be looking for as they add managers. Broadly speaking, across most segments of fixed income these reasons might include:

Substitutions in the event something goes wrong

Diversifying return drivers/profile

Enhancing returns (adding risk)

Non-investment alpha benefits

This means that managers not in that “core” position (and by “core” here I’m referring to the couple of managers in any given segment that are the most often used) the way to grow your business is to start with how clients are generally structuring their portfolios and the managers they are using and then focus your message on what your product and your firm are going to bring to the table. And remember: their primary worry is risk to the downside. How will you and your product help them?